QueenslandDutiesAct2001Current as at [Not

applicable]Indicative reprint noteThis is anunofficialversion of a

reprint of this Act that incorporates allproposedamendmentstotheActincludedintheRevenueandOtherLegislation

Amendment Bill 2018. This indicative reprint has been

preparedfor information only—it is not an

authorised reprint of the Act.The

point-in-time date for this indicative reprint is the introduction

date fortheRevenueandOtherLegislationAmendmentBill2018—22August2018.DetailedinformationaboutindicativereprintsisavailableontheInformationpage of the

Queensland legislation website.

Notauthorised—indicativeonlyPart

24668669670Part

25671672673674Schedule 2Schedule 3Schedule 4Schedule

4ASchedule 4BSchedule

4CSchedule 5Schedule 6Duties Act 2001Contents470Transitional provisions for Revenue

Legislation Amendment Act2018Definition for

part . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . .470Application of amendments increasing

the rate of AFAD. . . . . .470Application of amendments about rate of

vehicle registration duty471Transitional

provisions for Revenue and Other LegislationAmendment Act

2018Meaning of

amending Act. . . . . . . . . . . . . . . . . . . . . .

. . . . . . . .471Retrospective effect of ss

76E–76G. . . . . . . . . . . . . . . . . . . . .

.471Retrospective effect of amended s

179(4). . . . . . . . . . . . . . . . .472Retrospective effect of amended

definition business property. .472When

liability for transfer

duty on

dutiable transaction arises473Rates of duty on

dutiable transactions and

relevant acquisitions forlandholder and corporate trustee

duty. . . . . . . . . . . . . . . . . .479Example for partnership and trust

acquisitions and relevantacquisitions for corporate

trustees. . . . . . . . . . . . . . . . . . . . .480Amount of concession for

transfer duty—first home—residentialland. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .483Amount of

concession for transfer

duty—first

home—vacant

land484Rate of

vehicle registration duty other than for special vehicles485Example

for corporate reconstruction. . . . . . . . . . . . . . . . . .486Dictionary. . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . .488Page 31

Notauthorised—indicativeonly

Duties Act 2001Duties Act

2001Chapter 1 Introduction[s 1]An Act

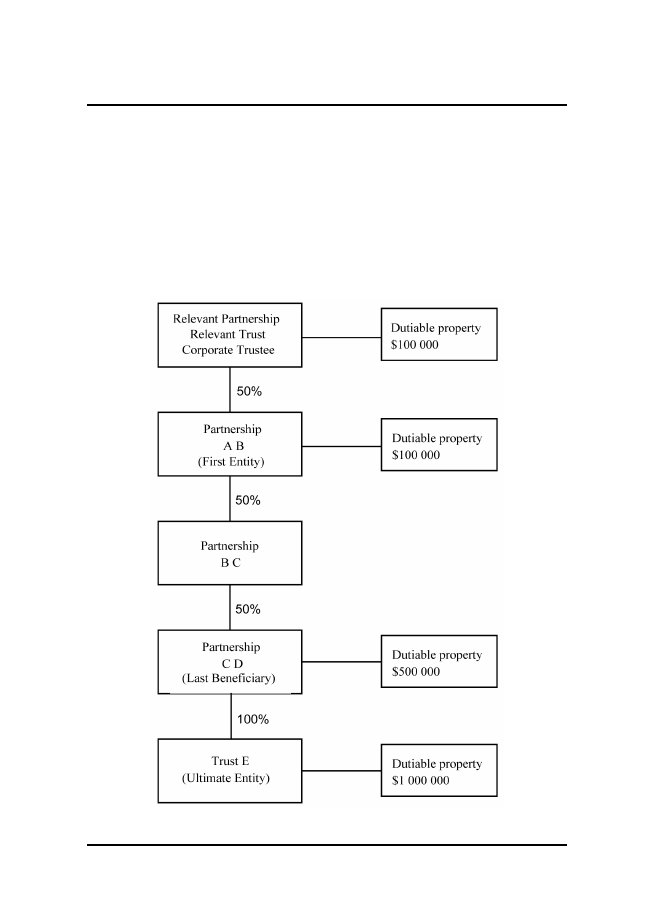

about creating and imposing dutiesNotauthorised—indicativeonlyChapter 1IntroductionPart 1Preliminary1Short

titleThis Act may be cited as theDuties Act 2001.2Commencement(1)ThisAct,otherthansections 306(2),342(2)and497,commences on a

day to be fixed by proclamation.(2)Sections 306(2), 342(2) and 497 commence on

the later of thefollowing—(a)a

day to be fixed by proclamation;(b)when

an arrangement is made under theCommonwealthPlaces (Mirror

Taxes) Act 1998(Cwlth), section 9, forQueensland.Part 2Interpretation3Definitions(1)The

dictionary in schedule 6 defines particular words used inthis

Act.Current as at [Not applicable]Page

33

Notauthorised—indicativeonlyDuties Act 2001Chapter 1

Introduction[s 5](2)The

definitionspousein schedule 6

applies despite theActsInterpretation

Act 1954, section 32DA(6).5Relationship of Act with Administration

Act(1)This Act does not contain all the

provisions about duties.(2)TheAdministrationActcontainsprovisionsdealingwith,among other

things, the following—(a)assessments of

duty;(b)collection and refunds of duty;(c)imposition of interest and penalty

tax;(d)objectionsandappealsagainst,orreviewsof,assessments of duty;(e)record keeping obligations of

taxpayers;(f)investigativepowers,offences,legalproceedingsandevidentiary matters;(g)service of documents;(h)registration of charitable

institutions.Note—Under the

Administration Act, section 3, that Act and this Act must beread

together as if they together formed a single Act.Part

3Application of Act6Act

binds all persons(1)This Act binds all persons, including

the State and, as far asthelegislativepoweroftheParliamentpermits,theCommonwealth and the other

States.Note—However, under

section 426, the State is exempt from duty unless thisAct

expressly provides otherwise.Page 34Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 7](2)Nothing in this Act makes the State liable

to be prosecuted foran offence.7Extra-territorial applicationThisActappliestoimposedutyoninstrumentsandtransactionsregardlessofwhethertheyareenteredintoormade in or outside Queensland.Note—This is because

instruments and transactions on which duty is imposedhave

a nexus to Queensland.7ADeclaration of

excluded matter for Corporations ActAninterestofapersoninaregisteredmanagedinvestmentschemeisdeclaredtobeanexcludedmatterfortheCorporationsAct,section 5F,inrelationtosection 1070A(1)(a), (3) and (4) of that

Act.Chapter 2Transfer

dutyPart 1Preliminary8Imposition of transfer duty(1)Thischapterimposesduty(transferduty)ondutiabletransactions.Notes—1Concessions and exemptions for

transfer duty are dealt with inparts 8A to 13.

Also, other exemptions are dealt with in chapter 10.2Additional foreign acquirer duty is

imposed on particular dutiabletransactions

under chapter 4.(2)Transfer duty is imposed on the

dutiable value of a dutiabletransaction.Current as at

[Not applicable]Page 35

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 9]Part 2Some

basic concepts fortransfer duty9What

is adutiable transaction(1)Each

of the following is adutiable transaction—(a)a transfer of

dutiable property;(b)anagreementforthetransferofdutiableproperty,whether conditional or not;(c)asurrenderofdutiablepropertythatislandinQueensland or a transferable site

area;(d)a vesting of dutiable property—(i)by, or expressly authorised by,

statute law of this oranotherjurisdiction,whetherinsideoroutsideAustralia;

or(ii)byacourtorder,ofthisoranotherjurisdiction,whether inside

or outside Australia;(e)a foreclosure of

a mortgage over dutiable property;(f)anacquisitionofanewrightonitscreation,grantorissue;(g)a

partnership acquisition;Note—Seechapter2,part7(Dutiabletransactionsrelatingtopartnerships).(h)thecreationorterminationofatrustofdutiableproperty;Note—See chapter 2,

part 8 (Dutiable transactions relating to trusts),division 3 (Creation and termination of

trusts).(i)a trust acquisition or trust

surrender.Page 36Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 10]Note—See

chapter 2, part 8 (Dutiable transactions relating to

trusts),division 4 (Some basic concepts about trust

acquisitionsandtrust surrenders).(2)It

does not matter whether a dutiable transaction—(a)is

effected by an instrument or another way; or(b)involves 1 or more parties.(3)Subsection (1) has effect subject to

sections 21, 29 and 37.Note—Under section

21, the commissioner must decide the applicable dutiabletransaction for imposition of duty if a

transaction constitutes more than1 type of

dutiable transaction mentioned in subsection (1).Also,forwhentransactions

forparticulardutiablepropertyarenotdutiable transactions, see sections 29

and 37.(4)Withoutlimitingsubsection (1)(d),propertyisvestedunderstatute law if the law vests property in an

entity that the lawstates is the successor in law of,

continuation of or same entityas, the entity

in which the property was previously vested.(5)However,propertyisnotvestedunderstatutelaw,ontheregistration of a company under the

Corporations Act, chapter5B, part 5B.1.10What

isdutiable property(1)Each

of the following isdutiable property—(a)land in Queensland;(b)a transferable site area;(c)an existing right;(d)a

Queensland business asset;(e)a chattel in

Queensland.Note—Section 498

includes provision about references to dutiable property.(2)A reference to property in subsection

(1) includes a referenceto an interest in the property, other

than the following—Current as at [Not applicable]Page

37

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 11](a)a

security interest;(b)a partner’s interest in the

partnership;(c)a trust interest;(d)the

interest of a discretionary object of a trust that holdsproperty mentioned in the subsection.Note—See theActs

Interpretation Act 1954, schedule 1, definitioninterest.11What is thedutiable

valueof a dutiable transaction(1)Thedutiable

valueof a statutory dutiable transaction is

theamount payable for the transaction.(2)Thedutiable

valueof a dutiable transaction that is a

partitionis determined under section 31.(3)Thedutiablevalueofadutiabletransactionthatisthesurrender of a

lease of land in Queensland is the total of anypremium,fineorotherconsiderationpayableforthesurrender.(4)Thedutiablevalueofadutiabletransactionthatistheacquisition of a

new right that is a lease of land in Queenslandis the total of

any of the following amounts payable for thelease—(a)premiums, fines or other consideration

payable for thegrant of the lease;(b)considerationpaidfor,orthevalueof,anymoveablechattelstakenoverbythelesseefromthelessororoutgoing lessee;(c)if,

on the leased premises, a business is to be carried onand

an amount in excess of what would be the rent if abusiness was not carried on is charged for

the lease—theexcess amount.(5)Thedutiablevalueofadutiabletransactionthatisapartnership

acquisition is determined under part 7, division 3.Page

38Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 12](6)Thedutiablevalueofadutiabletransactionthatisatrustacquisitionortrustsurrenderisdeterminedunderpart8,division 5.(6A)Thedutiablevalueofadutiabletransactionthatisanagreementforthetransferofdutiablepropertythatisafarm-in agreement is determined under

part 8A.(7)Subject to section 48, thedutiable valueof another

dutiabletransaction is—(a)the

consideration for the dutiable transaction; or(b)the

unencumbered value of the dutiable property or newright the subject of the transaction

if—(i)there is no consideration for the

transaction; or(ii)the

consideration can not be ascertained when theliability for

transfer duty arises; or(iii)theunencumberedvalueisgreaterthantheconsideration for the

transaction.(8)However, the dutiable value of

particular dutiable transactionsis subject to

apportionment under part 4.12Consideration for

dutiable transactions—general(1)The

consideration for a dutiable transaction includes—(a)theamountofanyliabilitiesassumedunderthetransaction, including an obligation,

whether contingentorotherwise,topayanyunpaidpurchasemoneypayable under an agreement for the transfer

of dutiableproperty; and(b)theamountorvalueofanydebttotheextentitisreleased or extinguished under the

transaction.(2)Iftheconsideration,oranypartoftheconsideration,foradutiable transaction on which duty is

imposed consists of anamount payable periodically and the

total amount, includingany interest, to be paid can be

ascertained, the considerationor part of the

consideration is the total amount.Current as at

[Not applicable]Page 39

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 13]Note—For

other provisions relevant to consideration, see sections 501 to

503.13Consideration for dutiable

transaction—transfer by wayof securityTheconsiderationforthetransferbywayofsecurityofdutiablepropertythatislandisanamountequaltotheunencumberedvalueofthedutiablepropertywhentheliability for transfer duty

arises.14What is theunencumbered

valueof property(1)Theunencumberedvalueofpropertyisthevalueoftheproperty determined without regard

to—(a)anyencumbrancetowhichthepropertyissubject,whether

contingently or otherwise; or(b)any

arrangement—(i)the parties to which are not dealing

with each otherat arm’s length; and(ii)thatresultsinthereductionofthevalueoftheproperty;

or(c)any arrangement for which a

significant purpose of anypartytothearrangementwas,inthecommissioner’sopinion, the

reduction of the value of the property.Example for

paragraph (c)—A owns land that B wishes to purchase. The

land is valued at$1m. Before the purchase, A grants B a 50

year lease of the land.B is not required to pay any rent

under the lease. A and B thenenter into an

agreement to transfer the land for $50,000, beingthe

value of A’s interest in the land taking into account that it

issubject to the lease to B.Theunencumberedvalueofthelandisdeterminedwithoutregard to the grant of the lease if the

commissioner is of theopinion there is an arrangement under

which A or B’s significantpurpose in entering into it was to

reduce the value of the land.Page 40Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 15](2)Also, theunencumbered

valueof property held on trust or byapartnershipmustbedeterminedwithoutregardtotheliabilities of the trust or

partnership, including for a trust, theliability to

indemnify the trustee.(3)Theunencumbered valueof property that

is the goodwill of abusinessincludesthevalueofanyrestraintoftradearrangement

entered into by the transferor or a related personof

the transferor to protect the value of the goodwill acquiredby

the transferee.(4)If, before a dutiable transaction

mentioned in section 9(1)(a),(b)or(d)forwhichthedutiablepropertyisland,improvementsaremadetothelandatthetransferee’sexpense,theunencumberedvalueofthelandmustbedetermined as if the improvements had not

been made.Note—Forprovisionsabouttheaggregateminimumvalueofthesharescomprising all

of the issued capital of a corporation or society and theunencumbered value of each of the shares,

see section 504.15When unencumbered value of property is

determinedThe unencumbered value of dutiable property

is determined—(a)foradutiabletransactionthatisthesurrenderoftheproperty—immediately before the surrender;

or(b)for another dutiable transaction—when

the liability fortransfer duty arises.Part 3Liability for transfer duty16When liability for transfer duty

arisesA liability for transfer duty imposed on a

dutiable transactionin schedule 2, column 1, arises at the

time stated opposite thetransaction in schedule 2, column

2.Current as at [Not applicable]Page

41

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 17]Note—In

relation to a dutiable transaction that is an ELN transfer or

ELNlodgement, see also sections 156H and

156K.17Who is liable to pay transfer

duty(1)Transferdutyimposedonastatutorydutiabletransactionmust be paid by

the statutory entity under the transaction.(2)Transfer duty imposed on another dutiable

transaction mustbe paid by the parties to the

transaction.18Need for instrument, ELN transaction

document orstatementIfadutiabletransactionisnoteffectedorevidencedbyaninstrument or ELN transaction

document, the parties liable topay transfer

duty on the transaction must make a statement inthe

approved form (atransfer duty statement) within the

timestated in section 19 for lodging the

statement.Maximum penalty—40 penalty units.19Lodging instrument, ELN transaction

document orstatement(1)Thestatutoryentityunderastatutorydutiabletransactionmust

lodge—(a)the instrument or ELN transaction

document that effectsor evidences the transaction;

or(b)the transfer duty statement for the

transaction.(2)The statutory entity must comply with

subsection (1)—(a)within 60 days after the liability

arises to pay transferduty on the transaction; or(b)if the amount payable for the

transaction is to be decidedby a court or

tribunal—within 14 days after the amountis

decided.Page 42Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 20](3)Thepartiesliabletopaytransferdutyrelatingtoanotherdutiabletransactionmust,within30daysaftertheliabilityarises,

lodge—(a)the instrument or ELN transaction

document that effectsor evidences the transaction or

transfer duty statementfor the transaction; and(b)an approved form for the

transaction.20Effect of making or lodging

instrument, ELN transactiondocument or

statement by 1 partyThe making of a transfer duty

statement, or the lodging undersection

19ofaninstrument,ELNtransactiondocumentortransferdutystatement,by1ofthepartiestothedutiabletransaction

relieves the other parties to the transaction fromcomplying with the requirement to make the

statement undersection 18 or lodge the instrument, ELN

transaction documentor transfer duty statement under

section 19.21No double duty—general(1)If a transaction for property

constitutes more than 1 dutiabletransaction for

the property and imposition of transfer duty onall of the

dutiable transactions for the property would result intransferdutybeingimposedmorethanonceonthetransaction,thecommissionermustdecidethedutiabletransaction on

which transfer duty is imposed.Notes—1For objections and appeals against

assessments of duty, see theAdministration

Act, part 6.2ForadutiabletransactionthatisanELNtransferorELNlodgement, see also part 15, division

2.(2)For subsection (1), the commissioner

must decide the dutiabletransactionthatisthemostapplicabledutiabletransactionhaving regard to

the provisions of this chapter and the primarypurpose of the

transaction.Current as at [Not applicable]Page

43

Duties

Act 2001Chapter 2 Transfer duty[s 22]Notauthorised—indicativeonly22No double

duty—particular dutiable transactions(1)Iftransferdutyisimposedonadutiabletransactionforperiodicalpaymentsofconsideration,nodutyisimposedunderthisActonanyagreementsecuringtheperiodicalpayments.(2)If transfer duty imposed on a dutiable

transaction that is anagreementforthetransferofdutiablepropertyispaid,notransfer duty is imposed on the transfer of

the property to thetransferee under the agreement.Note—For a dutiable

transaction that is an ELN transfer or ELN lodgement,see

also part 15, division 2.(2A)Also,ifapaymentcommitmentismadeforadutiabletransactionthatisanagreementforthetransferofdutiableproperty, no

transfer duty is imposed on an ELN transfer ofthe dutiable

property to the transferee under the agreement.Notes—1For a dutiable transaction that is an

ELN transfer, see also part 15,division

2.2See part 15, division 3 in relation to

the making of a paymentcommitment for an agreement for the

transfer of dutiable property.(3)If

the commissioner is satisfied—(a)a

person (theagent) is appointed

in writing as an agentfor another person (theprincipal); and(b)under the appointment, the agent

enters into a dutiabletransactionthatisanagreementforthetransferofdutiablepropertyfromaperson(theoriginaltransferor) to the agent

on behalf of the principal (theagreement);

and(c)theprincipalprovidedalltheconsideration,includingany

deposit paid; and(d)transfer duty imposed on the agreement

is paid; and(e)the dutiable property is later

transferred to the principalbytheoriginaltransferorortheagent(theagencytransfer);Page 44Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 23]no transfer duty

is imposed on the agency transfer or the trustacquisition or

trust surrender by the principal because of theagreement or

agency transfer.(4)For subsection (3)(a), the

commissioner must not be satisfiedthe person was

properly appointed as agent unless the originalinstrument of

appointment, or a copy of it, is lodged.(5)If—(a)thereisanagreementforthetransferofdutiableproperty

(thefirst agreement); and(b)afterthefirstagreementtakesplace,1ormoreagreements to transfer all or part of the

dutiable propertythesubjectofthefirstagreementtakesplace(theintervening

agreements); and(c)to

give effect to the first agreement and the interveningagreements, 1 or more transfers of dutiable

property (thetransfers) are effected

by 1 or more parties to the firstagreement and

the intervening agreements; and(d)transferdutyimposedonthefirstagreementandtheintervening

agreements is paid;no transfer duty is imposed on the

transfers.Example for subsection (5)—On 1

July, under an agreement for transfer, A agrees to sell land

inQueensland to B for $100,000. Settlement is

to take place on 31 July.On 7 July, under an agreement for

transfer, B agrees to sell the land to Cfor $120,000.

Again, settlement is to take place on 31 July. Before 31July, B directs A, that at settlement, A

transfer the land to C.The agreement between A and B is the

first agreement. The agreementbetween B and C

is the intervening agreement. No transfer duty isimposed on the transfer from A to C if

transfer duty on the first andintervening

agreements has been paid.23When credit to be

allowed for duty paid(1)If section

14(1)(c) is applied to determine the value of landbecause of a lease or occupancy right, in

assessing the transferduty payable for the dutiable

transaction that is the transfer, oragreementforthetransfer,oftheland,acreditmustbeCurrent as at [Not applicable]Page

45

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 24]allowed for any

lease duty paid under repealed chapter 4 forthe lease or

right.(2)Subsection (3) applies if—(a)transfer duty is paid on a dutiable

transaction that is anoptiontoacquiredutiableproperty(thefirsttransaction); and(b)on the exercise of the option,

transfer duty is payable onthedutiabletransactionfortheacquisitionofthedutiable property (thelater transaction); and(c)under the option, the consideration

paid for the option ispart of the consideration for the

later transaction.(3)In assessing the transfer duty on the

later transaction, a creditmustbeallowedforthetransferdutypaidforthefirsttransaction.(4)In

this section—repealed chapter 4means chapter 4

(Lease duty) as it was inforcefromtimetotimebeforeitsrepealbytheRevenueLegislation

Amendment Act 2005.24Rates of transfer

duty(1)Therateoftransferdutyimposedonadutiabletransactionthatisthetransfer,oranagreementforthetransfer,ofanexisting right

of a holder of the following is $5—(a)a

mortgage, including the debt secured by the mortgage,that

is solely over land in Queensland;(b)anothermortgage,includingthedebtsecuredbythemortgage,thatisincidentalto,andtransferredinconnection with, a mortgage mentioned in

paragraph (a)(aprimarymortgage)iftheprimarymortgageistheprincipal

security held by the transferor.(2)Therateoftransferdutyimposedonanotherdutiabletransactionisstatedinschedule 3,column2,oppositethedutiable value of the transaction in

schedule 3, column 1.Page 46Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 25]25Payment of transfer duty for deeds of grant

and particularfreeholding leases(1)This

section applies if transfer duty is imposed on a dutiabletransaction that is—(a)a

grant of land in fee simple under theLand Act

1994; or(b)anacquisitionofanewrightthatisapost-Wolfefreeholding

lease under theLand Act 1994.(2)Within30daysaftertheliabilityforthedutyarises,thegrantee or lessee must pay the duty to

the chief executive ofthe department in which theLand

Act 1994is administered.Part 4Apportionment ofconsideration

orunencumbered value forparticular

dutiable transactions26Apportionment—head office or principal place

ofbusiness in Queensland(1)Thissectionappliesfordeterminingtheconsiderationforadutiabletransactionfororrelatingto,ortheunencumberedvalue of,

dutiable property that is a Queensland business asset,otherthanadebtorpersonalproperty,ofaQueenslandbusiness that

has its head office or principal place of businessinQueenslandif,atanytimeduringthe3financialyearspreceding the dutiable transaction

concerned—(a)a supply of land, money, credit or

goods or any interestin them, or provision of services, has

been made by thebusiness to customers outside Queensland;

or(b)theassethasbeenused,exploitedorexercisedin,orrelates to, a place outside

Queensland.(2)A reference in this chapter to

consideration for the transactionor the

unencumbered value of the property is taken to be aCurrent as at [Not applicable]Page

47

Duties

Act 2001Chapter 2 Transfer duty[s 27]reference to the amount (theapportioned amount) worked

outusing the following formula—Notauthorised—indicativeonlywhere—AAmeans the apportioned amount.CUVmeans the consideration for the

dutiable transaction orunencumberedvalueoftheQueenslandbusinessassetmentioned in

subsection (1).OSmeans the gross amount of the supplies

and provision ofservices made by the business to its

customers in other Statesduring the 3 completed financial years

preceding the dutiabletransaction.TSmeansthegrossamountofsuppliesandprovisionofservices made by the business to all its

customers during the 3completed financial years preceding

the dutiable transaction.(3)However, the

commissioner may decide the consideration forthedutiabletransactionortheunencumberedvalueofthedutiablepropertyonanotherbasisifthecommissionerissatisfiedtheotherbasiswouldbemoreappropriateinparticular circumstances.27Apportionment—head office or principal

place ofbusiness in another State(1)Thissectionappliesfordeterminingtheconsiderationforadutiabletransactionfororrelatingto,ortheunencumberedvalue of,

dutiable property that is a Queensland business asset,otherthanadebtorpersonalproperty,ofaQueenslandbusiness that

does not have its head office or principal place ofbusiness in Queensland if, at any time

during the 3 financialyears preceding the dutiable

transaction concerned—(a)a supply of

land, money, credit or goods or any interestin them, or

provision of services, has been made by thebusiness to

customers in Queensland; orPage 48Current as at [Not applicable]

Duties Act 2001Chapter 2

Transfer duty[s 28](b)theassethasbeenused,exploitedorexercisedin,orrelates to, Queensland.(2)A reference in this chapter to

consideration for the transactionor the

unencumbered value of the property is taken to be areference to the amount (theapportioned amount) worked

outusing the following formula—Notauthorised—indicativeonlywhere—AAmeans the apportioned amount.CUVmeans the consideration for the

dutiable transaction orunencumberedvalueoftheQueenslandbusinessassetmentioned in

subsection (1).QSmeans the gross amount of the supplies

and provision ofservicesmadebythebusinesstoitsQueenslandcustomersduring the 3 completed financial years

preceding the dutiabletransaction.TSmeansthegrossamountofsuppliesandprovisionofservices made by the business to all its

customers during the 3completed financial years preceding

the dutiable transaction.(3)However, the

commissioner may decide the consideration forthedutiabletransactionortheunencumberedvalueofthedutiablepropertyonanotherbasisifthecommissionerissatisfiedtheotherbasiswouldbemoreappropriateinparticular circumstances.28Apportionment of particular dutiable

transactionsrelating to existing and new rights(1)This section applies for

determining—(a)theconsiderationforadutiabletransactionfororrelating to an existing right or

acquisition of a new righton its creation, grant or issue if the

right is exercisable orrelates to the conduct of a business

or activity outsideQueensland; orCurrent as at

[Not applicable]Page 49

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 29](b)the

unencumbered value of dutiable property that is anexisting right if the right is exercisable

or relates to theconduct of a business or activity outside

Queensland; or(c)the unencumbered value of a new right

on its creation,grant or issue if the right is exercisable

or relates to theconduct of a business or activity outside

Queensland.(2)A reference in this chapter to

consideration for the transactionortheunencumberedvalueoftherightistakentobeareference to the

amount that represents the same proportion oftheconsiderationorunencumberedvaluethattheunencumbered value of the right, to the

extent it is exercisableorrelatestotheconductofabusinessoractivityinQueensland,bearstothetotalunencumberedvalueoftheright.(3)However, the commissioner may decide

the consideration forthedutiabletransactionortheunencumberedvalueoftherightonanotherbasisifthecommissionerissatisfiedtheotherbasiswouldbemoreappropriateinparticularcircumstances.Part 5Dutiable transactions relatingto

dutiable property29When transaction for chattel is not

dutiable transaction(1)If a chattel in

Queensland is the subject of a transaction, thetransaction is

not a dutiable transaction unless—(a)anothertypeofdutiablepropertyisthesubjectofthesame

transaction; or(b)undersection

30,itisaggregatedwithadutiabletransaction that

is not for a chattel.(2)For subsection

(1)(b), section 30 applies as if the transactionwere

a dutiable transaction.Page 50Current as at

[Not applicable]

Duties Act 2001Chapter 2

Transfer duty[s 30]Notauthorised—indicativeonly30Aggregation of dutiable

transactions(1)Thissectionappliestodutiabletransactionsthattogetherform,evidence,giveeffecttoorarisefromwhatis,substantially 1 arrangement.(2)Forassessingtransferdutyoneachofthedutiabletransactions,

the transactions must be aggregated and treatedas a single

dutiable transaction.Example for subsection (2)—A

conducts a business of manufacturing bullbars. A agrees to sell

thebusinesstoBasagoingconcernfor$50,000,000.Thepropertyincludedintheagreementcomprisesland,plantandequipment,goodwill and the

business name.The land is dutiable property being land in

Queensland and each of theother assets are dutiable property

being Queensland business assets.The agreement,

so far as it relates to the sale of the land, is a dutiabletransaction being an agreement to transfer

land in Queensland and, sofar as it relates to the agreement to

sell each of the business assets, is adutiable

transaction being an agreement to transfer dutiable propertythat

is a Queensland business asset. Accordingly, there are 4

dutiabletransactions under the agreement.Because the dutiable transactions together

form 1 arrangement, theymust be aggregated under this section

for imposing transfer duty.(3)For

subsection (1), all relevant circumstances relating to thedutiable transactions must be taken into

account in decidingwhether they together form, evidence, give

effect to or arisefrom what is, substantially 1

arrangement.(4)Forsubsection

(3),relevantcircumstancesincludethefollowing—(a)whether the transactions are contained in 1

instrument;(b)whether any of the transactions are

conditional on entryinto, or completion of, any of the

other transactions;(c)whetherthepartiestoanyofthetransactionsarethesame;(d)whether any party to a transaction is a

related person ofanother party to any of the other

transactions;(e)the time over which the transactions

take place;Current as at [Not applicable]Page

51

Duties

Act 2001Chapter 2 Transfer duty[s 30]Notauthorised—indicativeonly(f)whether, before

the transactions take place, the dutiablepropertythesubjectofthetransactionswasusedtogether,ordependentlywithoneanother,bythetransferor or transferors;(g)whether,afterthetransactionstakeplace,thedutiablepropertythesubjectofthetransactionswillbeusedtogether,ordependentlywithoneanother,bythetransferee or transferees.(5)Transfer duty imposed on the dutiable

transaction aggregatedunder this section must—(a)beassessedonthetotalofthedutiablevaluesofthetransactions when the liability for

transfer duty for eachof the transactions arose; and(b)be apportioned between the

transactions as decided bythe commissioner.Example for

subsection (5)—Under 4 agreements between a builder and a

developer, the builderagrees to purchase 4 lots of land from

the developer for $100,000 each.The lots are

dutiable property being land in Queensland and each of theagreements is a dutiable transaction being

an agreement to transfer landin

Queensland.Even though the sale of the 4 lots was

negotiated at the same time, theagreements were

signed on different dates over a 10 month period, haddifferent settlement dates and were not

conditional on each other.Under section 24 (Rates of transfer

duty) and schedule 3 (Rates of dutyon dutiable

transactions and relevant acquisitions for landholder andcorporatetrusteeduty),theagreementsforlots1to3havebeenseparately

stamped for $2350 transfer duty. When the agreement for lot4 is

lodged for stamping, the commissioner decides this section

appliesbecause the transactions together formed 1

arrangement.Accordingly, the transactions must be

aggregated under this section forimposing

transfer duty and the duty apportioned between them.Under subsection (5)(a), the total of the

dutiable values of the dutiabletransactions on

which transfer duty is imposed is $400,000, being thevalue of each of the lots when the liability

for transfer duty arose foreach of the

transactions, regardless of a variation in the values since

theliability arose.Undersection 24andschedule 3,transferdutyimposedontheaggregated

transaction is $12,475.Page 52Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 31]Ifthecommissionerdecidestoapportionthetransferdutyequallybetween the

dutiable transactions, the amount of transfer duty payableis

$3118.75 for each transaction.Under the

Administration Act, part 3, the commissioner will make areassessment for the transactions for lots 1

to 3. The assessment noticemust state the

matters mentioned in section 26(2) of that Act.(6)Eachpartytoeachofthedutiabletransactionsmust,whenlodging the

instrument, ELN transaction document or transferduty

statement relating to the transaction, give notice to thecommissioner stating details known to the

party about—(a)all of the dutiable property included

or to be included inthe arrangement mentioned in

subsection (1); and(b)the dutiable value of each dutiable

transaction.Note—Under the

Administration Act, the requirement under this subsection isa

lodgement requirement for which a failure to comply is an

offenceunder section 121 of that Act.(7)Thissectiondoesnotapplytoadutiabletransactiontotheextent that it relates to an exchange

of dutiable property.31Partitions(1)This section applies to a dutiable

transaction under which thefollowing

happens (thepartition)—(a)dutiable property held by persons

jointly as joint tenantsor tenants in common (each aco-owner) is

transferred,oragreedtobetransferred,to1ormoreoftheco-owners;(b)thedutiablepropertytransferred,oragreedtobetransferred, includes the interest

held by the transfereein the property immediately before the

transaction.(2)The dutiable value of the dutiable

transaction is the greater ofthe

following—(a)theamountbywhichtheunencumberedvalueofthedutiablepropertytransferred,oragreedtobetransferred, is more than the

unencumbered value of theCurrent as at [Not applicable]Page

53

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 32]interestheldbythetransfereeinthepropertyimmediately

before the transaction;(b)the

consideration paid by any party to the transaction.(3)Thissectiondoesnotapplytoatransactionifsection 48applies to the

transaction.32Transfer by way of

security—land(1)This section applies if the

commissioner is satisfied—(a)there has been a

dutiable transaction that is a transfer ofdutiablepropertybywayofsecurity(theoriginaltransfer); and(b)the property is land; and(c)transfer duty has been paid on the

transaction; and(d)thepropertyhasbeenretransferredtothepersonwhotransferred it by way of security

(theretransfer) or hasbeen

transferred to a person to whom the property hasbeentransmittedbydeathorbankruptcy(alsotheretransfer).(2)The commissioner must make a

reassessment of transfer dutypaid on the

original transfer to reduce the duty to the amountthat

would have been payable if the amount secured by thetransfer had been secured by a mortgage for

which mortgageduty were imposed.(3)Transfer duty is not imposed on the dutiable

transaction that isthe retransfer.(4)Subsection (2)appliestothereassessmentdespitethelimitationperiodundertheAdministrationActforreassessments.Note—See

the Administration Act, part 3 (Assessments of tax), division

3(Reassessments).Page 54Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 33]33Transfer by way of security—other dutiable

property(1)Transfer duty is not imposed on a

dutiable transaction if—(a)the transaction

is a transfer of dutiable property by wayof security;

and(b)the property is not land.(2)Subsection (3) applies if—(a)after the transfer by way of security,

the transferee, orthetransferee’sassignee,acquiresownershipofthedutiable

property free from any interest of the transferor,or

transferor’s assignee; and(b)thetransferee,orthetransferee’sassignee,weretonewlyacquirethedutiablepropertyatthetimeoftheacquisition

mentioned in paragraph (a), the acquisitionwould be a

dutiable transaction.(3)The acquisition

of the ownership of the dutiable property bythe transferee

is taken to be a dutiable transaction and transferdutyimposedonthetransactionmustbereducedbytheamount of mortgage duty, if any, paid

on the transfer.Part 6Special

provisions aboutdutiable transactions relatingto

Queensland business assetsDivision 1Some basic

concepts aboutQueensland businesses and theirassets34What

is aQueensland business assetAQueenslandbusinessassetisabusinessassetofaQueensland

business.Current as at [Not applicable]Page

55

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 35]35What

is abusiness asset(1)Each

of the following is abusiness asset—(a)goodwill;(b)astatutorybusinesslicenceusedforcarryingonabusiness;(c)arighttouseastatutorybusinesslicenceusedforcarrying on a business;(d)the

business name used for carrying on a business;(e)a

right under a franchise arrangement used for carryingon a

business;(f)a debt of a business if the debtor

resides in Queensland;(g)a supply right

of a business;(h)intellectual property used for

carrying on a business;(i)personal

property in Queensland of a business.(2)For

subsection (1)—(a)abusinessassetmentionedinsubsection (1)(b)thatisissued or given under—(i)aQueenslandActisusedforcarryingonabusiness; or(ii)aCommonwealthActisusedforcarryingonabusinessifitisused,exploitedorexercisedinQueensland; and(b)another business asset is used for carrying

on a businessif it is used, exploited or exercised in

Queensland.36What is aQueensland

businessAQueensland businessis a

business—(a)that is conducted on or from a place

in Queensland; or(b)theconductofwhichconsistswhollyorpartlyofsupplying land, money, credit or goods or

any interest inPage 56Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 37]them,orprovidinganyservice,toQueenslandcustomers;

or(c)that has ceased but satisfied

paragraph (a) or (b) at anytime in the 1

year before a dutiable transaction that is thetransfer, or

agreement for the transfer, of an asset of thebusiness.Example for paragraph (c)—Abusiness conductedfromaplaceinQueenslandgoesintoliquidation.

Three months after the business stops trading, theliquidatortransfersbusinessassetsofthebusiness.Fordeterminingwhetherthetransferofthebusinessassetsisadutiabletransaction,thebusinessisaQueenslandbusinessbecauseparagraph

(a)was satisfied in the 1 year beforethetransfer.Division 2Transactions for particular assets ofQueensland businesses37When

transaction for particular Queensland businessassets not

dutiable transaction(1)Ifadebtofabusinessthatisevidencedbyanegotiableinstrument is

the subject of a transaction, the transaction is nota

dutiable transaction unless—(a)anothertypeofdutiablepropertyisthesubjectofthesametransactionor,undersection

30,itisaggregatedwith a dutiable

transaction; or(b)under the transaction, the negotiable

instrument is or istobetransferredwithall,orsubstantiallyall,ofthenegotiable

instruments of the business.(2)If a

supply right of a business is the subject of a transaction,the

transaction is not a dutiable transaction unless—(a)anothertypeofdutiablepropertyisthesubjectofthesametransactionor,undersection

30,itisaggregatedwith a dutiable

transaction; orCurrent as at [Not applicable]Page

57

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 38](b)underthetransaction,thesupplyrightisoristobetransferredwithall,orsubstantiallyall,ofthesupplyrights of the business.(3)If

intellectual or personal property of a business is the

subjectof a transaction, the transaction is not a

dutiable transactionunless, under section 30, it is

aggregated with 1 or more of thefollowing—(a)a

dutiable transaction for a Queensland business asset,other than intellectual or personal

property;(b)a dutiable transaction for land in

Queensland.(4)For subsections (1)(a), (2)(a) and

(3), section 30 applies as ifthe transaction

were a dutiable transaction.38When

consignment of trading stock of Queenslandbusiness is a

dutiable transaction(1)This section

applies if—(a)the owner of a Queensland business

transfers or agreestotransferaQueenslandbusinessasset,otherthantradingstockofthebusiness,toaperson(thenewowner); and(b)theownerplacesallormostofthetradingstockonconsignmentforsalebyaperson,whetherornotthenewowner,(theconsignee)intheconductofthebusiness by the

new owner; and(c)havingregardtothetermsoftheconsignmentitisreasonable to conclude that the

consignment is, or is partof, an arrangement to avoid transfer

duty.(2)Withoutlimitingsubsection (1)(c),thetermsoftheconsignment include the

following—(a)the amount payable to the owner by the

consignee andthe terms of payment;(b)the

price ultimately payable to the owner for the tradingstock and the way in which it is worked

out;(c)the basis of working out the

consignee’s commission;Page 58Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 39](d)the

right of the consignee to mix the trading stock withother property not owned by the

owner;(e)the right of the consignee to deal

with the trading stockas if it were the consignee’s or other

than as agent of theowner.(3)The

placing of the trading stock on consignment is taken to bea

transfer of the stock.Note—Accordingly, the

transfer is a dutiable transaction being the transfer of aQueensland business asset because trading

stock is a business assetbeing personal property.39Surrender of Queensland business asset

so replacementasset may be granted(1)ThissectionappliesifaQueenslandbusinessassetissurrendered by a person (theowner) so that a

similar businessasset may be granted, issued, given to or

obtained by anotherperson.(2)For

imposing transfer duty—(a)thesurrenderistakentobeatransferofthebusinessasset by the owner to the other person when

the similarbusiness asset is granted, issued, given or

obtained; and(b)the owner and other person are the

parties to the dutiabletransaction that is the transfer of

the business asset.Current as at [Not applicable]Page

59

Duties

Act 2001Chapter 2 Transfer duty[s 40]Part

7Dutiable transactions relatingto

partnershipsNotauthorised—indicativeonlyDivision 1Preliminary40Interpretation for property held by

partnership or trustAreferencetoapartnershiportrustholdingpropertyisareference to the holding of the

property by the partners for thepartnership or

trustees on trust.Division 2Some basic

concepts aboutpartnership acquisitions41What

is apartnership acquisitionApersonmakesapartnershipacquisitionifthepersonacquires a

partnership interest in a partnership that—(a)holds dutiable property; or(b)has an indirect interest in dutiable

property.Note—Section 498

includes provision about references to dutiable property.42What is a partner’spartnership interest(1)A

partner’spartnership interestis—(a)ifthepartnerhasavariablepartnershipentitlementundersubsection (2)—theproportionthatthevalueofthe

partner’s entitlements as a partner bears to the valueoftheentitlementsofallpartnersinthepartnershipexpressed as a

percentage; or(b)if the partner is entitled only to

share in the profits of thepartnershipandhasgivenorisrequiredtogiveconsideration,orhasmadeorisrequiredtomakeaPage

60Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 43]contributiontothecapitalofthepartnership,fortheacquisitionoftheprofit-sharingright—thepartner’sprofit-sharing

percentage; or(c)if paragraph (a) or (b) does not

apply—the greater of thefollowing—(i)the

percentage of the capital of the partnership thepartner has contributed or is obliged to

contribute;(ii)the percentage

of the losses of the partnership thepartner is

required to bear.(2)Forsubsection

(1)(a),apartnerhasavariablepartnershipentitlementinapartnershipif,intheordinarycourseofdetermining the partner’s entitlement to

share in the profits orobligationtocontributetothecapitalorlossesofthepartnership, the entitlement or

obligation varies or may varyfrom time to

time.43What is a partnership’sindirect interestin

dutiablepropertyA partnership

has anindirect interestin dutiable

property if—(a)through a partnership interest or

trust interest there is aconnectionbetweenthepartnershipanddutiableproperty of the

other partnership or trust; or(b)through a series of partnership interests or

trust interests,or a combination of any of them, there is a

connectionbetweenthepartnershipanddutiablepropertyofapartnership or

trust in the series.44Acquiring a partnership

interest(1)Apersonacquiresapartnershipinterestifapartnershipisformed or the person’s partnership interest

increases.(2)Without limiting subsection

(1)—(a)a partnership may be formed on—(i)a change in the membership of a

partnership; orCurrent as at [Not applicable]Page

61

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 45](ii)the

merger of 2 or more partnerships; or(b)a

person’s partnership interest may increase—(i)under the terms of a partnership agreement;

or(ii)on the

retirement of a partner from a partnership;or(iii)onachangeinthetermsofapartnershipagreement

effecting a change in the interests of thepartners.(3)However,apartner’svariablepartnershipentitlementundersection 42 does not increase if—(a)thepartner’sentitlementtoshareintheprofitsorobligationtocontributetothecapitalorlossesofthepartnershipincreasesmerelybecauseofthepartner’sperformance as a partner; and(b)there is no arrangement

stating—(i)theextentofthefuturevariationtothepartner’sentitlement or

obligation; or(ii)the

consideration for the variation.Division 3Dutiable value of partnershipacquisitions45What

is the dutiable value of a partnership acquisitionThe

dutiable value of a partnership acquisition is the greaterof

the following—(a)theconsiderationfortheacquisitionsofarastheconsideration relates to dutiable property,

or an indirectinterest in dutiable property, held by the

partnership;(b)the value of the acquisition worked

out under section 46or 47.Page 62Current as at [Not applicable]

Duties Act 2001Chapter 2

Transfer duty[s 46]Notauthorised—indicativeonly46What is the value of a partnership

acquisition—general(1)Subject to subsections (5) and (6),

the value of a partnershipacquisition is the total of the

amounts worked out by applyingthe partner’s

partnership interest to the unencumbered value,when the

liability for transfer duty arises, of—(a)thedutiablepropertyheldbythepartnership(therelevant partnership); and(b)anyindirectinterestindutiablepropertyheldbytherelevant partnership.(2)For subsection (1)(b), the

unencumbered value of an indirectinterest under

section 43(a) of the relevant partnership is theamount worked out by applying to the

unencumbered value ofthe dutiable property held by the

entity in which the relevantpartnership has

a partnership or trust interest, the partnershipor

trust interest of the relevant partnership in that entity.(3)For subsection (1)(b), the

unencumbered value of an indirectinterest under

section 43(b) of the relevant partnership is theamount worked out by—(a)first applying to the unencumbered value of

the dutiableproperty held by the ultimate entity, the

partnership ortrust interest of the partnership or trust

(thelast partnerorbeneficiary)thatisapartnerorbeneficiaryoftheultimate entity; and(b)applying to the amount worked out

under paragraph (a),andtheunencumberedvalueofanydutiablepropertyheld by the last

partner or beneficiary, the partnership ortrust interest

of the next partnership or trust in the seriesof partnerships

or trusts that is a partner or beneficiaryof the last

partner or beneficiary; and(c)applying the calculation in paragraph (b)

for each of theotherpartnershipsortrustsintheseriesuntilthefirstentity’s

partnership interest or trust interest is used in thecalculation; and(d)applying to the amount last worked out under

paragraph(c) and the unencumbered value of any

dutiable propertyCurrent as at [Not applicable]Page

63

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 47]held by the

first entity, the partnership or trust interest ofthe

relevant partnership.(4)Schedule

4containsanexampleofhowthevalueofapartnership

acquisition is worked out.(5)Fordeterminingthevalueofanewpartner’spartnershipacquisitiononformationofapartnership,thevalueofanydutiable property the partner

contributed to the partnership onits formation

must be disregarded.(5A)For subsection

(5), a person is a new partner only if—(a)the

person was not in partnership with any partners ofthe

partnership immediately before its formation; or(b)ontheperson’spartnershipacquisition,thepersonbecomesapartnerinanadditionalpartnershiptoapartnershipinwhichthepersonisapartnerwithanypartnersoftheadditionalpartnershipimmediatelybefore its

formation.(5B)However,

subsection (5A)(b) does not apply to a person whomakesapartnershipacquisitioninapartnershipthatwasformed because of a change in the

membership of the partnersof another partnership (theold

partnership) if the person hada partnership

interest in the old partnership.(6)Fordeterminingthevalueofapartner’spartnershipacquisitionthatisanincreaseinthepartner’spartnershipinterest,thepartner’spartnershipinterestistakentobetheincrease in the

partner’s partnership interest.47What

is the value of a partnership acquisition—merger of2 or

more partnerships(1)This section applies if—(a)aperson(thepartner)firstmakesapartnershipacquisition(thenewpartnershipacquisition)onthemerger of 2 or

more partnerships; andPage 64Current as at

[Not applicable]

Duties Act 2001Chapter 2

Transfer duty[s 47]Notauthorised—indicativeonly(b)thepersonhadapartnershipinterest(theoldpartnership interest) in 1 of the

merging partnerships;and(c)the

partner were to make a partnership acquisition fortheoldpartnershipinterestimmediatelybeforethemerger, the value of the partnership

acquisition wouldinclude all or part of the unencumbered

value of dutiableproperty(thecontinuingproperty)thatbecomesdutiable property of the merged

partnership.(2)The value of the new partnership

acquisition must be reducedby the lesser

of—(a)theamountthatwouldbethevalueofthenewpartnershipacquisitionifthedutiablepropertyofthemergedpartnershipcomprisedonlythecontinuingproperty;

or(b)theamountthatrepresentsthevalueofthepartner’spartnershipacquisitionfortheoldpartnershipinterestmentionedinsubsection (1)(c)immediatelybeforethemergerworkedoutasifthedutiablepropertyoftheformerpartnershipcomprisedonlythecontinuingproperty.Example for working out dutiable value under

this section—X is a 30% partner in the XYZ partnership

that has dutiable property of$10m. The XYZ

partnership merges with another partnership, to form anew

partnership (the merged partnership). X has a 40%

partnershipinterest in the merged partnership. The

merged partnership has dutiableproperty with an

unencumbered value of $12m, including $2m of thedutiable property of the XYZ partnership

(the continuing property).ThevalueofX’snewpartnershipacquisitionisworkedoutasfollows—Example—1The value of X’s

interest in the merged partnership is $4.8m, being40%

(X’s partnership interest in the merged partnership) of $12m(theunencumberedvalueofthemergedpartnership’sdutiableproperty).2The

reduction under subsection (2)(a) is $800,000, being 40%

(X’spartnershipinterestinthemergedpartnership)of$2m(thecontinuing

property).Current as at [Not applicable]Page

65

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 48]3The

reduction under subsection (2)(b) is $600,000, being 30%

(X’spartnershipinterestintheXYZpartnership)of$2m(thecontinuing

property).The value of X’s partnership acquisition is

$4.2m, being $4.8m less$600,000whichisthelesseroftheamountsworkedoutundersubsection

(2).Division 4Dutiable value

of other dutiabletransactions for dutiable property ofpartnership48Dutiable value of dutiable transaction

reduced fortransfer of dutiable property to partner on

retirement ordissolution(1)Thissectionappliesif,onaperson(theretiringpartner)ceasing to be a partner in a partnership

because of the retiringpartner’sretirementfromthepartnershiporitsdissolution,dutiable

property of the partnership is transferred or agreed tobe

transferred to the retiring partner.(2)The

dutiable value of the dutiable transaction for the transfer,or

agreement for the transfer, of the dutiable property to theretiring partner must be reduced by an

amount worked out byapplyingtheretiringpartner’spartnershipinterestinthepartnershiptotheunencumberedvalueofthedutiableproperty immediately before the retirement

or dissolution.Example for subsection (2)—A,BandCareinpartnershipinequalshares.Bhadaone-thirdpartnership

interest immediately before retiring. On B ceasing to be apartner, A and C transfer land to B. The

dutiable value of the landacquired by B will be reduced by

one-third.Page 66Current as at

[Not applicable]

Notauthorised—indicativeonlyPart

8Duties Act 2001Chapter 2

Transfer duty[s 49]Dutiable

transactions relatingto trustsDivision 1Preliminary49Application of pt 8(1)Thispartappliestoallexpresslyorintentionallycreatedtrusts, regardless of how they are

created.(2)However, this part does not apply to a

trust acquisition or trustsurrender of a trust interest in a

public unit trust other than amajority trust

acquisition in a land holding trust.Notes—1For subsection (2), see division 7

(Public unit trusts), subdivisions7 (Majority

trust acquisitions in land holding trusts) and 8 (Indirecttrust interests).2Anacquisitionofaninterestinalistedunittrustthatisalandholder may

be dutiable under chapter 3, part 1 (Landholderduty).50Joint trusteesIf a trust has 2

or more trustees, the trustees are taken to be asingle person for this chapter.Note—Under section

65, trustees are jointly and severally liable for transferduty

payable.Current as at [Not applicable]Page

67

Duties

Act 2001Chapter 2 Transfer duty[s 51]Division 2Some basic

concepts aboutpropertyNotauthorised—indicativeonly51Interpretation

for property held by trust or partnershipAreferencetoatrustorpartnershipholdingpropertyisareference to the holding of the

property by the trustees on trustor the partners

for the partnership.52Contracted property and trust

interests(1)For a trust, contracted property is

taken to be dutiable propertyheld by the

trust.(1A)If a trust has

made a purchase or sale agreement for a trustinterest, the

trust is taken to have an indirect interest in thetrust-related dutiable property.(2)Fordeterminingthedutiablevalueofatrustcreation,trusttermination, trust acquisition or trust

surrender—(a)a sale agreement made by the trustee

is taken not to havebeen made; and(b)apurchaseagreementmadebythetrusteeistakentohave

been completed.(3)Subsection (3A) applies if—(a)contractedproperty,oranindirectinterestindutiablepropertymentionedinsubsection (1A),isincludedindetermining the dutiable value of a trust

creation, trusttermination, trust acquisition or trust

surrender; and(b)afterwards, the sale agreement for the

property or trustinterest is completed or the purchase

agreement for theproperty or trust interest is not

completed.(3A)Thecommissionermustmakeareassessmentasifthecontracted

property or indirect interest were never held by thetrust.(4)For

the reassessment, the parties liable to pay transfer duty onthe

trust creation, trust termination, trust acquisition or

trustPage 68Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 53]surrender must

lodge the instruments required for the originalassessment.(5)In

this section—purchaseagreementincludesanuncompletedagreement,whetherornotconditional,fortheacquisitionofatrustinterest through

which the trust would have, if the agreementwere completed,

an indirect interest in dutiable property (thetrust-related

dutiable property).sale agreementincludes an

uncompleted agreement, whetheror not

conditional, for the disposal of a trust interest throughwhichthetrusthasanindirectinterestindutiableproperty(also thetrust-related

dutiable property).Division 3Creation and

termination of trusts53Creating trust of

dutiable property(1)A trustofdutiablepropertyis

createdifaperson,whohasacquiredpropertyotherthanastrustee,startstoholdtheproperty as trustee.(2)Also, a trust of dutiable property is

created if all the followingapply—(a)a person holds dutiable property on

trust (trust 1);(b)the person is also trustee of another

trust (trust 2);(c)the person ceases to hold the dutiable

property as trusteeoftrust1andstartstoholdthedutiablepropertyastrustee for trust 2;(d)when the person starts to hold the

dutiable property astrustee for trust 2—(i)a person who has a trust interest for

the dutiableproperty under trust 2 did not have a trust

interestfor that property when it was held for trust

1; or(ii)a person who has

a trust interest for the dutiableproperty under

trust 2 had a trust interest for thatCurrent as at

[Not applicable]Page 69

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 54]propertywhenitwasheldfortrust1andthatperson’s trust

interest increases.Note—Section 498

includes provision about references to dutiable property.54Terminating trust of dutiable

propertyA trust of dutiable property is terminated

if a person, havingheld the property as trustee, starts to hold

the property otherthan as trustee.Division 4Some

basic concepts about trustacquisitions and trust

surrenders55What is atrust

acquisitionA person makes atrust

acquisitionif the person acquires atrust interest

in a trust that—(a)holds dutiable property; or(b)has an indirect interest in dutiable

property.Note—Under section

81, an indirect trust acquisition in a land holding trust istakentobeatrustacquisition.Anindirecttrustacquisitionistheacquisition of an interest in a land

holding trust through 1 or morecorporations,

partnerships or trusts, or a combination of any of them.See

definitionsindirect trust acquisitionandindirect trust interestinthe dictionary.56What

is atrust surrenderA person makes

atrust surrenderif the person

surrenders atrust interest in a trust that holds

dutiable property or has anindirect

interest in dutiable property.Page 70Current as at [Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 57]57What

is atrust interest(1)Atrustinterestisaperson’sinterestasabeneficiaryofatrust, other than a life

interest.(2)For a trust that is a discretionary

trust, only a taker in defaultof an

appointment by the trustee can have a trust interest.(3)Also, for a trust that is a

superannuation fund, a member of thefund has a trust

interest in the fund.Note—For exemption

from transfer duty for a trust acquisition or surrender ofa

member’s interest in a superannuation fund, see section 119.58What is a trust’sindirect

interestin dutiable propertyA trust has

anindirect interestin dutiable

property if—(a)through a trust interest or

partnership interest, there is aconnectionbetweenthetrustanddutiablepropertyofthe other trust or partnership;

or(b)through a series of trust interests or

partnership interests,or a combination of any of them, there

is a connectionbetweenthetrustanddutiablepropertyofatrustorpartnership in the series.59Acquiring a trust interest(1)A person acquires a trust interest

if—(a)the person becomes a beneficiary of a

trust, whether oncreation of the trust or otherwise;

or(b)being a beneficiary of a trust, the

person’s trust interestincreases, other than because of the

surrender of anotherperson’s trust interest in the trust

for which transfer dutyhas been paid.(2)If a

beneficiary’s trust interest is subject to a prior life

interest,the interest does not increase merely

because the life tenantdies or, over time, the extent of the

life interest reduces.Current as at [Not applicable]Page

71

Duties

Act 2001Chapter 2 Transfer duty[s 60]Notauthorised—indicativeonly60Beneficiary’s

trust interest is percentage of orproportionate to

property held on trust(1)A beneficiary’s

trust interest is—(a)forabeneficiarywhoisatakerindefaultunderadiscretionary trust—(i)the percentage of the trust income or

trust propertythebeneficiarywouldreceiveindefaultofappointment by the trustee; or(ii)if the

beneficiary would receive both trust incomeand trust

property in default of appointment by thetrustee, the

greater percentage of the trust incomeor trust

property the beneficiary would receive; or(b)forabeneficiaryofatrust,otherthanadiscretionarytrust,whoseentitlementissolelytoincomeoftheproperty held on trust—the proportion

that the value ofthebeneficiary’sentitlementbearstothevalueoftheentitlementsofallbeneficiariesexpressedasapercentage;

or(c)foranotherbeneficiary—theproportionthatthebeneficiary’sentitlementunderthetrustbearstotheunencumberedvalueofthepropertyheldontrustexpressed as a

percentage.(2)For subsection (1)(c), the

beneficiary’s entitlement under thetrust is—(a)the amount of the unencumbered value

of the propertyheldontrustthatthebeneficiarycouldreceiveasaresult of the acquisition of the

beneficiary’s trust interestdetermined at

the time of acquisition of the interest; or(b)the

entitlement stated in subsection (3) if—(i)the

beneficiary’s entitlement under the trust is notsubject to a prior life interest; and(ii)thebeneficiary’sentitlementunderthetrustmayincrease, including from nothing, on the

fulfilmentofanycondition,contingencyortheexerciseornon-exercise of any power or discretion;

andPage 72Current as at

[Not applicable]

Notauthorised—indicativeonlyDuties Act 2001Chapter 2

Transfer duty[s 61](iii)the

condition, contingency, power or discretion ispartofanarrangementasignificantpurposeofwhich is to lessen the amount of the

beneficiary’sentitlement at a particular time.(3)For subsection (2)(b), the

beneficiary’s entitlement under thetrust is the

maximum interest in the property held on trust thatthe

beneficiary would have on the fulfilment of the conditionor

contingency or the exercise or non-exercise of the power ordiscretion.(4)For

a majority trust acquisition, a reference in this section to

abeneficiary’sentitlementunderthetrustincludestheentitlementunderthetrustofrelatedpersonsofthebeneficiary.61Who

is arelated person(1)A

person is arelated personof another

person if—(a)for individuals—they are members of

the same family;or(b)foranindividualandacorporation—thepersonoramember of the

person’s family is a majority shareholder,director or

secretary of the corporation or a related bodycorporate of the

corporation, or has an interest of 50% ormore in it;

or(c)for an individual and a trustee—the

person or a relatedpersonunderanotherprovisionofthissectionisabeneficiary of

the trust; or(d)for corporations—they are related

bodies corporate; or(e)foracorporationandatrustee—thecorporationorarelated person under another provision

of this section isa beneficiary of the trust; or(f)for trustees—(i)there is a person who is a beneficiary of

both trusts;orCurrent as at [Not applicable]Page

73

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 62](ii)apersonisbeneficiaryof1trustandarelatedperson under

another provision of this section is abeneficiary of

the other trust.(2)Also,apersonisarelatedpersonofanotherpersonifthepersons acquire

trust interests in a land holding trust and theacquisitions

form, evidence, give effect to or arise from whatis

substantially 1 arrangement.(3)However, a person is not arelated personof another

personundersubsection

(1),otherthansubsection (1)(d),ifthecommissioner is satisfied the trust

interests of the persons in aland holding

trust—(a)were acquired, and will be used,

independently; and(b)were not acquired, and will not be

used, for a commonpurpose.Division 5Dutiable value of trust acquisitionsand

trust surrenders62What is the dutiable value of a trust

acquisition or trustsurrenderThe dutiable

value of a trust acquisition or trust surrender isthe

greater of the following—(a)the

consideration for the acquisition or surrender so faras

the consideration relates to dutiable property, or anindirect interest in dutiable property, held

by the trust;(b)thevalueoftheacquisitionorsurrenderworkedoutunder section 63.63What

is the value of a trust acquisition or trust surrender(1)Subjecttosubsections (6)to(8),thevalueofatrustacquisitionortrustsurrenderisthetotaloftheamountsworked out by applying the beneficiary’s

trust interest to thePage 74Current as at

[Not applicable]

Duties Act 2001Chapter 2

Transfer duty[s 63]Notauthorised—indicativeonlyunencumberedvalue,whentheliabilityfortransferdutyarises, of—(a)thedutiablepropertyheldbythetrust(therelevanttrust);

and(b)anyindirectinterestindutiablepropertyheldbytherelevant trust.Note—Undersection

52(1),dutiablepropertyincludescontractedproperty.Also, under section 52(1A), the relevant

trust may be taken to hold anindirect

interest in dutiable property through a trust interest that is

thesubject of a purchase or sale

agreement.(2)For subsection (1), the beneficiary’s

trust interest for a trustsurrender is the beneficiary’s trust

interest immediately beforethe

surrender.(3)For subsection (1)(b), the

unencumbered value of an indirectinterest under

section 58(a) of the relevant trust is the amountworkedoutbyapplyingtotheunencumberedvalueofthedutiable

property held by the entity in which the relevant trusthasatrustorpartnershipinterest,thetrustorpartnershipinterest of the

relevant trust in that entity.(4)For

subsection (1)(b), the unencumbered value of an indirectinterest under section 58(b) of the relevant

trust is the amountworked out by—(a)first applying to the unencumbered value of

the dutiablepropertyheldbytheultimateentity,thetrustorpartnership interest of the trust or

partnership (thelastbeneficiary or

partner) that is a beneficiary or partner ofthe

ultimate entity; and(b)applying to the

amount worked out under paragraph (a),andtheunencumberedvalueofanydutiablepropertyheldbythelastbeneficiaryorpartner,thetrustorpartnership interest of the next trust or

partnership in theseriesoftrustsorpartnershipsthatisabeneficiaryorpartner of the last beneficiary or partner;

and(c)applying the calculation in paragraph

(b) for each of theothertrustsorpartnershipsintheseriesuntilthefirstCurrent as at

[Not applicable]Page 75

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 63]entity’s trust

interest or partnership interest is used in thecalculation;

and(d)applying to the amount last worked out

under paragraph(c) and the unencumbered value of any

dutiable propertyheld by the first entity, the trust or

partnership interest ofthe relevant trust.(5)Schedule 4 contains an example of how

the value of a trustacquisition is worked out.(6)For determining the value of a

beneficiary’s trust acquisitionthat is an

increase in the beneficiary’s trust interest, other thana

majority trust acquisition, the beneficiary’s trust interest

istaken to be the increase in the

beneficiary’s trust interest.(7)Subsection (8) applies to a majority trust

acquisition that is anincreaseinabeneficiary’strustinterest(therelevanttrustacquisition)thathashappenedinthefollowingcircumstances—(a)the

trust interest of the beneficiary and related personsof

the beneficiary was 50% or more immediately beforethe

relevant trust acquisition;(b)transferdutywaspreviouslypaidforamajoritytrustacquisitioninthetrustmadebythebeneficiaryorrelated persons;(c)sincethemajoritytrustacquisitionmentionedinparagraph (b), no other related person

of the beneficiaryhas made a trust acquisition in the

trust.(8)For determining the value of the

beneficiary’s trust acquisitionthatistherelevanttrustacquisition,thebeneficiary’strustinterest is taken to be the increase in the

beneficiary’s trustinterest.Page 76Current as at [Not applicable]

Division 6Duties Act

2001Chapter 2 Transfer duty[s 64]Liability to transfer dutyNotauthorised—indicativeonly64Liability to pay transfer duty on

creation or termination oftrust(1)Ifatrustofdutiablepropertyiscreatedorterminated,thetrustee of the trust is the party to the

dutiable transaction thatis the creation or termination of the

trust.(2)If the trustee of the trust does not

pay the transfer duty, thebeneficiaries of the trust are jointly

and severally liable for theduty.65Liability of joint trusteesIf a

trust has 2 or more trustees, the trustees are jointly andseverally liable for any transfer duty

imposed.66When no transfer duty on trust

acquisition or trustsurrender(1)If,

because of the creation of a trust of dutiable property, aperson acquires a trust interest in the

property, transfer duty isnot imposed on the acquisition

if—(a)transfer duty has been paid for the

dutiable transactionthat is the creation of the trust of

the property; or(b)the dutiable transaction that is the

creation of the trust ofthe property is exempt from transfer

duty.(2)If, because of the acquisition of

dutiable property by a trust, aperson acquires

a trust interest in the property, transfer duty isnot

imposed on the acquisition of the trust interest if—(a)the trustee has paid transfer duty for

the acquisition ofthe property; or(b)thedutiabletransactionthatistheacquisitionoftheproperty is exempt from transfer duty;

or(c)duty is not imposed on the acquisition

of the property bythe trustee.Current as at

[Not applicable]Page 77

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 67](3)If,

because of the termination of a trust of dutiable property,

aperson surrenders a trust interest in the

property, transfer dutyis not imposed on the surrender

if—(a)transfer duty has been paid for the

dutiable transactionthat is the termination of the trust

of the property; or(b)thedutiabletransactionthatistheterminationofthetrust of the property is exempt from

transfer duty.67Parties to trust acquisition and trust

surrender(1)Foratrustacquisition,thebeneficiaryacquiringthetrustinterest is the

party to the dutiable transaction.(2)Foratrustsurrender,thetrusteeandthebeneficiarywhosetrustinterestissurrenderedarethepartiestothedutiabletransaction.Note—Under section 17, the parties to a dutiable

transaction are liable to paytransfer duty

imposed on the transaction.Division 7Public unit trustsSubdivision

1Preliminary68What

is apublic unit trustApublic unit trustis—(a)a listed unit trust; or(b)a widely held unit trust; or(c)a wholesale unit trust; or(d)a pooled public investment unit trust;

or(e)a declared public unit trust.Page

78Current as at [Not applicable]

Notauthorised—indicativeonlySubdivision 2Duties Act

2001Chapter 2 Transfer duty[s 69]Basic concepts about listed unittrusts69What

is alisted unit trustAlisted unit trustis a unit trust

the units in which are quotedon the market

operated by a recognised stock exchange.Notes—1Section 498Aincludesprovisionaboutwhenthequotationofsecurities is suspended.2Anacquisitionofaninterestinalistedunittrustthatisalandholder may

be dutiable under chapter 3, part 1 (Landholderduty).Subdivision 3Basic concepts

about widely heldunit trusts70What

is awidely held unit trust(1)Awidely held unit trustis a

unit trust, other than a listed unittrust,thatisaregisteredmanagedinvestmentschemeforwhich—(a)units in the trust have been issued to the

public; and(b)50 or more persons are beneficially

entitled to the unitsin the trust; and(c)more

than 20 persons are beneficially entitled to at least75%

of the total units in the trust.Note—Also, under section 71, the commissioner may

treat a unit trust as awidely held unit trust.(2)However, for a trust acquisition or

trust surrender of a trustinterest in a trust, a unit trust is

not a widely held unit trust ifsubsection

(1)(b) and (c) is not satisfied before and after thetrust acquisition or trust surrender.Current as at [Not applicable]Page

79

Notauthorised—indicativeonlyDuties Act 2001Chapter 2 Transfer

duty[s 71](3)For

subsection (2), a trust acquisition or trust surrender of atrustinterestinaunittrustincludesaseriesoftrustacquisitions or

trust surrenders under an arrangement.(4)If

subsection (2) applies to a unit trust, the trust is not a

widelyheld unit trust from immediately before the

trust acquisition ortrust surrender or the first

acquisition or surrender under thearrangement.(5)For

subsection (1), a person is taken to be beneficially

entitledtoallunitsheldbythepersonandrelatedpersonsoftheperson.71When unit trust may be treated as

widely held unit trust(1)This section

applies if the commissioner is satisfied—(a)units in a unit trust (thestart up units) will be issued

tothepublictoanextentandwiththeentitlementsmentioned in

section 70(1) within 1 year after the firstissue of units

to the public; and(b)the start up units are the only units

in the unit trust to beissuedfromandincludingthefirstissuetothepublicuntil the unit trust becomes a widely held

unit trust (thestart-up period).(2)The commissioner may treat the unit

trust as a widely heldunit trust for the start-up

period.(3)However,ifthestart-upunitsarenotissuedinthewaymentioned in subsection (1)(a) or are not

the only units issuedintheunittrustinthestart-upperiod(thedisqualifyingcircumstances)—(a)the trustee must, within 28 days after

the disqualifyingcircumstanceshappen,givethecommissionernoticeabout the disqualifying circumstances;

and(b)the unit trust is taken not to have

been a widely held unittrust in the start-up period;

and(c)the commissioner must make an

assessment for transferduty for each trust acquisition or

trust surrender in thePage 80Current as at

[Not applicable]